Sainsbury’s Balance Transfers allow you to move existing credit card debt to a new card with a temporary 0% interest period.

This guide explains the fee structure, promotional duration, and repayment conditions associated with these offers.

You will learn how to assess total costs and decide whether this option fits your financial situation.

Understanding How Sainsbury’s Balance Transfers Work

Sainsbury’s Balance Transfers allow you to move existing credit card debt to a new Sainsbury’s Bank credit card.

The goal is to reduce interest costs during a promotional 0% period and create a structured repayment plan.

- Transfer Existing Debt – You move outstanding balances from other eligible credit cards to your Sainsbury’s card, subject to approval and credit limit.

- Pay a One-Time Transfer Fee – Most offers include a percentage-based fee, calculated from the total amount transferred.

- Benefit from a 0% Promotional Period – You pay no interest on the transferred balance for a fixed number of months, as long as you meet the terms.

- Make Minimum Monthly Payments – You must pay at least the required minimum each month to maintain the promotional rate.

- Standard APR Applies After Promotion – If any balance remains after the 0% period ends, the representative APR will apply to the remaining amount.

- Credit Assessment Required – Approval depends on your credit profile, income, and affordability checks.

Who Can Apply

Understanding the eligibility requirements is essential before submitting an application to Sainsbury’s Bank.

Approval is based on creditworthiness, affordability checks, and standard lending criteria.

- UK Residency – Applicants must be permanent UK residents with a valid residential address.

- Minimum Age Requirement – Applicants must be at least 18 years old at the time of application.

- Good Credit Standing – A stable credit history with no recent serious defaults or insolvency issues is expected.

- Regular Income – Evidence of consistent income is necessary to meet affordability assessments.

- No Restricted or Delinquent Accounts – Existing accounts in arrears or under restriction may affect eligibility.

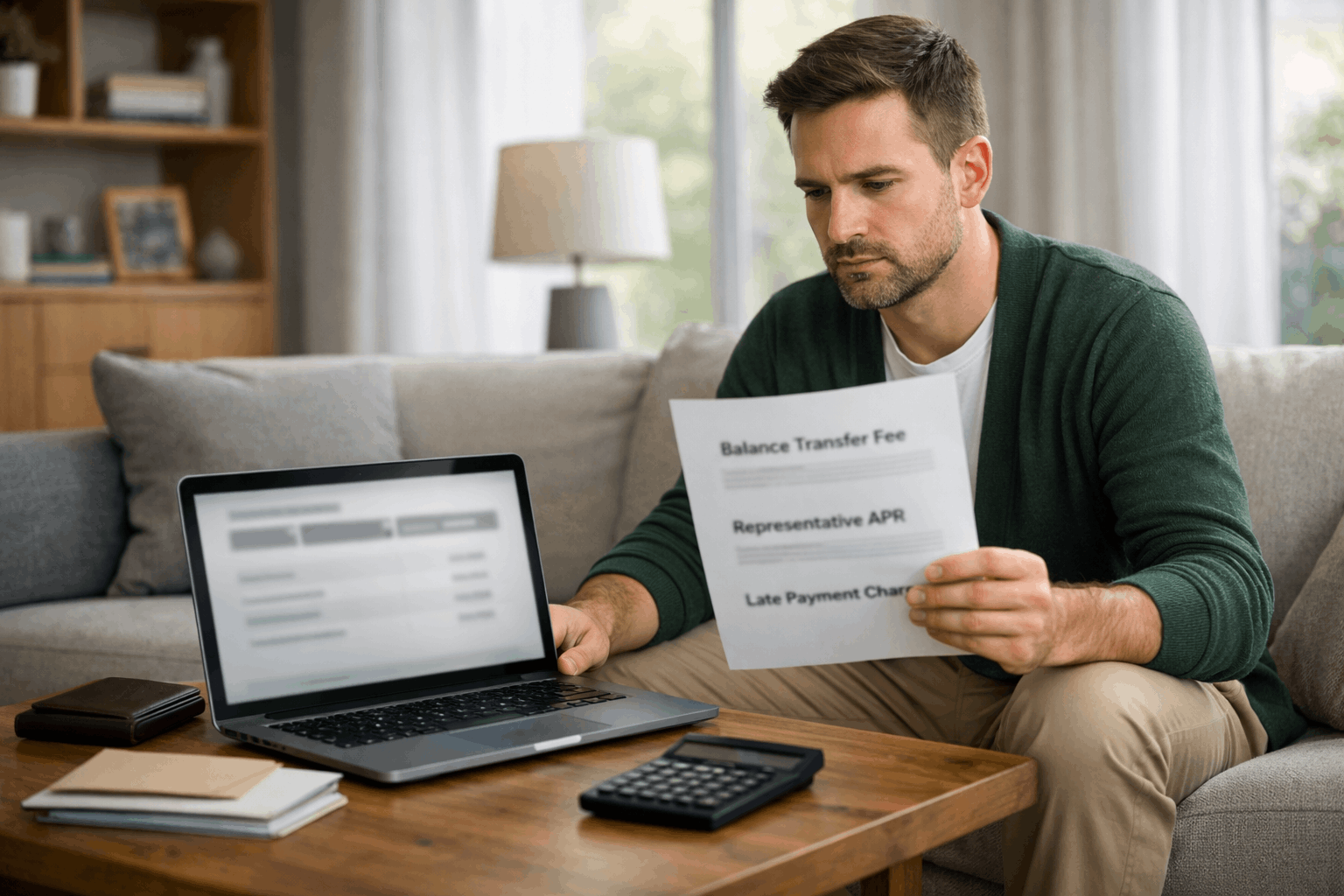

Fee Structure Explained

Understanding the total cost is essential before choosing Sainsbury’s Balance Transfers.

Specific figures, including transfer fees and representative APR, should always be verified directly with Sainsbury’s Bank, as rates may change.

- Balance Transfer Fee (Around 1%–3% or More) – A one-time percentage fee is charged on the amount transferred, depending on the offer.

- Representative APR (Varies by Card) – After the 0% period ends, any remaining balance is charged at the standard APR.

- Late Payment Fee – Missing a payment may trigger a late charge, subject to UK regulatory limits.

- Over-Limit Fee – Going over the approved credit limit may result in an additional fee.

- Cash Advance and Transaction Fees – Cash withdrawals and similar transactions often carry higher interest and separate charges.

Duration Options for 0% Balance Transfers

The promotional length determines how long interest is not charged on the transferred balance.

Exact durations should be verified with Sainsbury’s Bank, as offers are subject to change.

- Short-Term Offers (e.g., 6–12 Months) – Shorter 0% periods may come with lower transfer fees and suit faster repayment plans.

- Mid-Term Offers (e.g., 12–24 Months) – Moderate durations provide more time to repay while balancing fee costs.

- Long-Term Offers (e.g., 24–30+ Months) – Longer 0% periods give extended repayment time but may include higher fees.

- Duration vs. Fee Trade-Off – Longer promotional periods often mean higher fees, so a total cost comparison is essential.

Minimum Payment Rules and Promotional Conditions

Maintaining the 0% promotional rate depends on following the card’s payment terms.

All conditions should be reviewed carefully with Sainsbury’s Bank before proceeding.

- Minimum Monthly Payment Required – At least the stated minimum amount must be paid each month by the due date.

- On-Time Payments Only – Missing or late payments may result in loss of the promotional rate.

- No Breach of Credit Limit – Exceeding the approved limit can affect promotional terms.

- Promotion Withdrawal Risk – The 0% offer may be withdrawn if account terms are not followed.

Application Process Overview

Applying for a balance transfer with Sainsbury’s Bank requires a formal credit application and assessment.

This process can influence the overall credit profile depending on account management.

- Check Eligibility – Use the online tool to review potential approval without immediate commitment.

- Complete the Application – Submit personal, employment, and financial details for assessment.

- Credit Assessment – A full credit check is conducted before a decision is made.

- Request the Balance Transfer – Provide details of the existing card and the amount to transfer.

- Receive Confirmation – Once approved, the balance is transferred within the stated timeframe.

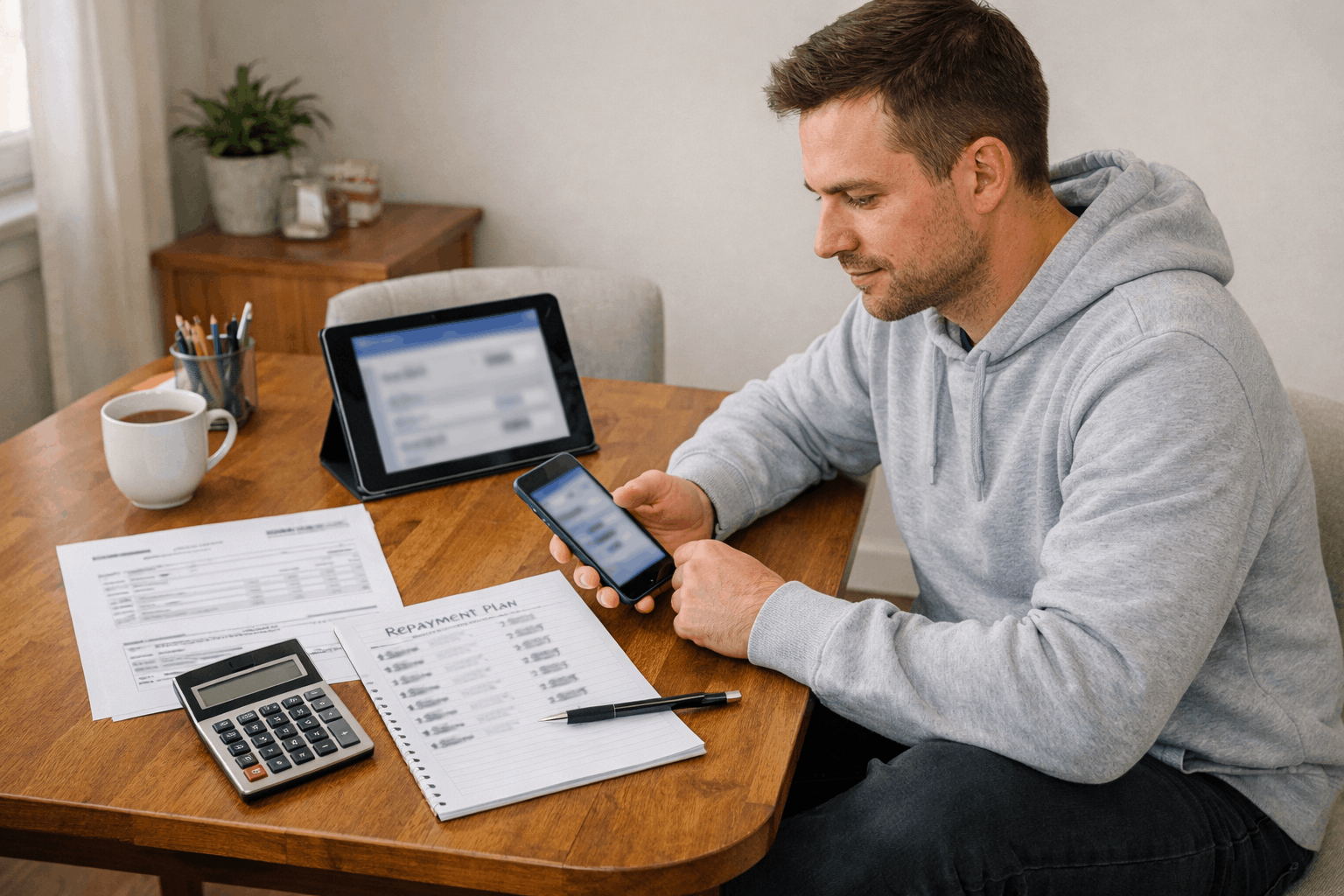

Repayment Strategy During the Promotional Period

Clearing the balance within the 0% period helps avoid standard interest charges.

A structured repayment plan increases the chances of finishing before the promotion ends.

- Divide the Balance by Months – Split the total transferred amount by the number of promotional months to estimate a monthly target payment.

- Pay More Than the Minimum – Paying only the minimum extends the balance, so higher payments reduce risk.

- Set Up Direct Debit – Automatic payments help maintain on-time repayment and protect the promotional rate.

- Track Remaining Balance – Regularly review statements to ensure progress toward clearing the debt.

How Balance Transfers Affect Your Credit Score

Applying for a balance transfer can influence your credit profile in several ways. The impact depends on borrowing behaviour and overall account management.

- Hard Credit Search – A full application usually involves a hard inquiry, which may temporarily lower the score.

- New Account Opening – Opening a new credit card can affect the average age of accounts.

- Credit Utilisation Changes – Transferring balances may improve the utilisation ratio if managed carefully.

- Payment History Impact – Consistent, on-time payments can strengthen the overall credit record.

Contact Information

Here’s verified contact information for Sainsbury’s Bank.

You should always verify the details on the official website before using them, as they may change over time.

- General Customer Support Phone – 0345 788 8444 (UK number for support inquiries).

- Credit Card Assistance – Support information available through the bank’s credit card help pages (check FAQs online first).

- Data Protection / Privacy Queries (Email) – [email protected].

- General Email Contact – [email protected] (for complaints and general enquiries).

- Postal Address (Privacy/Data Protection) – Data Protection Officer, Sainsbury’s Bank, 1 New Park Square, Edinburgh Park, Edinburgh, EH12 9GR.

Make an Informed Decision Before Transferring Your Balance

Sainsbury’s Balance Transfers can reduce interest costs when the fee structure and promotional duration are clearly understood.

Careful planning, on-time payments, and reviewing the representative APR after the 0% period are essential for managing total cost.

Review the latest terms on the official Sainsbury’s Bank website and compare offers before making a final decision.

Disclaimer

This information is for educational purposes only and does not constitute financial advice.

Terms, fees, and interest rates may change, so always verify the latest details directly with Sainsbury’s Bank before applying.